Part of our Accounting Concepts guide

What Are Accounting Estimates?

Accounting Estimate is a technique to measure those items in accounting that have no accurate quantification and are therefore estimated based on judgment and knowledge derived from experience. . They involve certain elements in the financial statements whose value cannot be determined using objective data.

However, those transactions are also necessary for maintaining proper details in the books of accounts for future reference. Thus, even though uncertainties and values must be determined using historical estimates and approximations, they should also be a part of financial reporting. A well-supported estimation will lead to a transparent and reliable financial statement.

Accounting Estimates Explained

The concept of accounting estimate deals with judgement or making approximations regarding some financial transactions in the books of accounts. The value of such element cannot be always fixed based of any particular data. They usually involve a lot of uncertainties and therefore some expertise, skill and knowledge is required to determine the value, which will always be an approximation.

Such inherent uncertainty arise due to differences in valuation, measurement or the method followed in the recognition process of revenues, liabilities, assets and various expenses. Such cases require significant accounting estimates.

This also leads to the fact that there is a certain level of subjectivity in the process because the management and accountants require a very good level of skill, expertise and knowledge to make the assumption. Thus, there is an obvious situation where there will be differences in the value assumed for such items which will be based on the information available from various sources.

Such estimates are also subject to changes over time due to change in economic and accounting policies, revision in assumptions and new information coming in. It is extremely necessary for companies to record and take these changes into consideration so that they are clearly reflected in the financial statements and reports.

Typically the note to the financial statements contain the details of the basis of assumptions and estimates and the methods followed of the same. Such disclosures are necessary to maintain transparency and accountability. Therefore the management should use their best available judgement for the critical accounting estimates.

Types

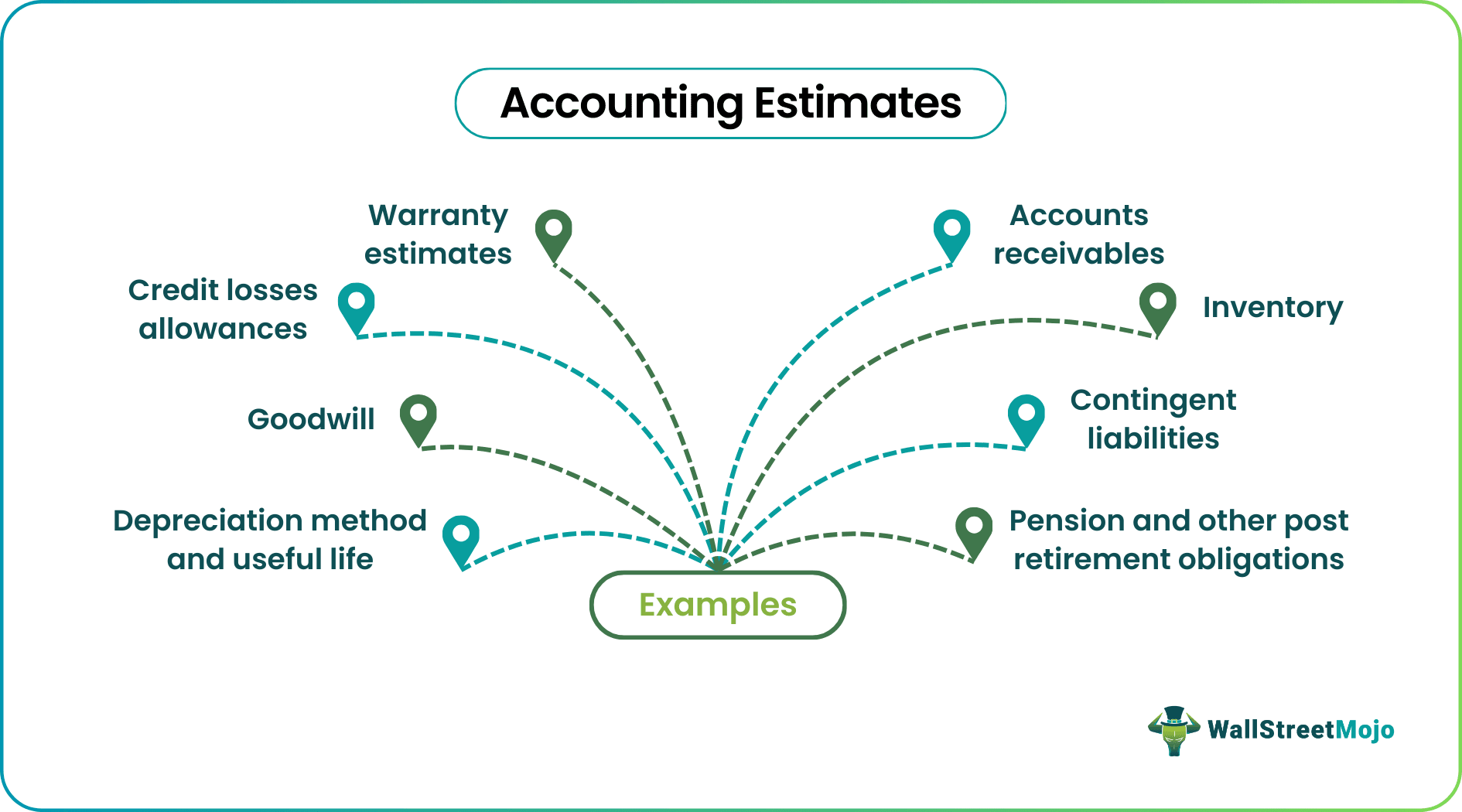

Here are the top 8 list of significant accounting estimates examples –

#1 – Accounts Receivables

Accounts Receivables are one of the most common examples. As we see below, Ligand considers receivables past due based on contractual payment terms of 30 to 90 days.

source: Ligand SEC Filings

#2 – Inventory

Ligand valued inventory based on FIFO and is stated at lower of cost or market value. Obsolete inventory is accessed periodically, and inventory write-downs are done to their net realizable value.

source: Ligand SEC Filings

#3 – Depreciation Method and Useful Life

Ligand uses the straight-line method for depreciation method and considers the useful life in three to ten years.

source: Ligand SEC Filings

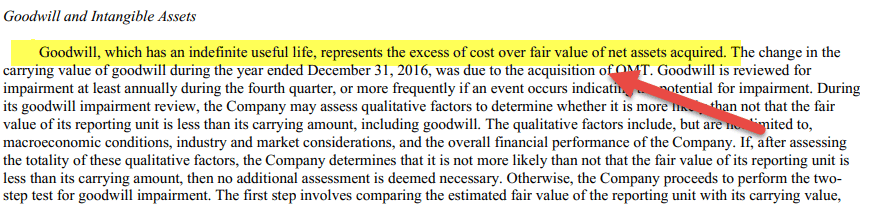

#4 – Goodwill

Goodwill has an indefinite useful life. A goodwill impairment review is done annually to assess any changes in goodwill.

source: Ligand SEC Filings

#5 – Contingent Liabilities

Contingent liabilities for Ligand were $4.97 million. Contingent liabilities are again subjective critical accounting estimates. Many inputs are considered here, including revenue volatility, the probability of commercialization of the product, timings, thresholds, etc.

source: Ligand SEC Filings

#6 – Warranty Estimates

Companies that provide warranties have to establish warranty-related costs. Ford forecasts these warranty and field service action obligations using a patterned estimation model, as described below.

# 7 – Pension and Other Post Retirement Obligations

To estimate the Pension Cost and other post-retirement obligations, companies have to estimate the discount rate, expected long-term return on the plan assets, salary growth, inflation, retirement rates, mortality rates, etc.

#8 – Credit Losses Allowances

The credit loss is the change in the provision for credit losses at prior period exchange rates. For analysis purposes, Ford management splits the provision for credit losses into net charge-offs and the change in the allowance for credit losses.

source: Ford SEC Filings

Example

Let us try to understand the concept with the help of a suitable example.

Let’s say that a company perceives that it will incur some bad debts during a particular period. But, it has no idea how many bad debts it will incur during the period. The question is how much provision the company should create to be able to deal with the bad debts? Can the company deliberately calculate the bad debts in quantifiable measures?

The answer is the bad debts the company is about to incur can’t be measured in numbers. The accountant, who would be creating the provisions for the bad debts, needs to depend on his judgment and expertise to conclude. And then, he would create a provision entirely from his experience and years of training.

This particular measurement through which few items in accounting are quantified is called accounting estimates.

Video Explanation Of Accounting Estimates

Why Is Accounting Estimates Important?

Significant accounting estimates may not seem very significant, but actually, it is a great way to prove the company’s worth to the investors.

But why is this so very important?

Because in this case, the accountants need to put in more effort.

When there’s no quantifying opportunity for the accountants, they need to look for more information. They gather many data points, use their experience, see the historical data, and then value the items on the list since the actual amount for the particular items is unknown.

We will talk about a couple of items to make things clear.

- Depreciation: How would one understand how much depreciation a company should incur for machinery or a plant? Yes, one can use the accounting method; but there’s no accurate information about how much should be the written down value at the end of every year. That’s why it’s the accountant’s job to determine how much percentage of depreciation should be incurred by the company by looking at the life expectancy of the plant or machinery and then by seeing the usefulness and necessity of the machinery for the business.

- The useful life of fixed assets: It’s difficult to say how long fixed assets will serve a company. How would a company know how long it will serve the company if a machine is purchased? Well, there’s no possible quantifiable method. The accountant needs to use an accounting estimate to figure out the useful life of fixed assets. The accountant needs to look at past data points, look at the similar machinery in similar companies, and finally use their knowledge and expertise to figure out an significant accounting estimates of the useful life of fixed assets.

Purpose

Since the accountant can’t just debit or credit any account without the precise amount, accounting estimates need to be done to get an estimate of the same account. For example, let’s say that depreciation would be debited for machinery the company has just bought. Without the precise amount, the accountant wouldn’t be able to put it on the debit side.

To pass that journal entry, the accountant needs to estimate an approximate amount, and then she can pass the entry.

Audit Procedures

It is a big question. When an auditor looks at the financial statements and accounting entries, they have one question: Do the entries/items have evidence to support them?

In the case of all other accounting entries, the company can produce evidence.

But in the case of items where the accountants have used an accounting estimate, the company can’t have any physical evidence.

That’s why for the auditors, the list of accounting estimates aren’t very convincing. Things like management bias, subjective assumptions, or errors in judgment may affect the estimates.

When an auditor is looking at the accounting statements and the accounting entries, he should be very careful and ensure that the amounts estimated based on accounting estimates are free from bias, errors, and wrong assumptions.

As an investor, you should take the same approach.

If you’re new to investing, you may need to educate yourself in the fundamentals and advanced accounting to discover errors in accounting estimates.

But for the investors who have many years of experience would be able to judge the entries quite well. Yes, like auditors, these investors wouldn’t have all the information. But if they know the fundamentals of accounting; they would be able to judge the basics like –

- Whether the percentage of depreciation taken is right? (as an investor, you can look at similar companies and compare)

- Is the provision for bad debts right? (You can see what that company did in the previous years and also how similar companies in the same industry respond to bad debts)

- How many years of useful life has that company estimated for its fixed assets? (find out the past data points and how the company has used the same previously)

These questions may seem a bit advanced for an investor, but an actual story lies between the lines. Suppose an investor wants to invest a decent amount in the company. In that case, it makes sense to look at the financial statements and the accounting entries with diligence, meticulousness, and closer examination.

And there lies the importance of correctness and accuracy in disclosing the financial statements of the company.

Accounting Estimates Vs Accounting Policies

The above are two different financial concepts that are commonly used while preparing financial statements for a company. However, it is necessary to understand the basic differences between the two. Let us point out the same, as given below:

- The list of accounting estimates refers to judgements or approximations that the business has to make for transactions whose value cannot be determined in a definite manner, but the latter refers to procedures and principles that the business should follow while preparing the financial statements and reporting.

- In the former, information related to historical data, opinions and knowledge of experts, etc are used for achieving useful results, whereas in case of the latter, the guidelines are provided by various company laws and policymakers based on which decisions are taken.

- The former is subjective in nature because of their dependence in expert knowledge, skill and experience, which also rely on the information available from various sources during a particular time. The latter is more objective in nature because the rules and policies are fixed and for each reporting period which should also be disclosed in the financial statements.

- The former is subject to changes since they depend on various other external factors and subjective in nature. But the policies remain the same for a long time period, unless some new information comes in or there is some change in economic policies.

Thus, both are important and relevant in the financial world and should be used to maintain consistency, transparency and provide a clear view of the financial condition of the business.

Recommended Articles

This article has been the guide to Accounting Estimates and their definition. Here we discuss the list of accounting estimates along with examples and explanations. You may also have a look at the below-recommended articles on accounting.