Table Of Contents

What Is Full Disclosure Principle?

Full Disclosure Principle is an accounting policy backed by GAAP (Generally Accepted Accounting Principles) and IFRS7 (International Financial Reporting Standards), which requires the management of an organization to disclose every relevant and material financial information.

The information may be related to monetary or non-monetary, to creditors, investors and any other stakeholder who depends on the financial reports published by the organization in their decision-making process related to the organization. The disclosure principle is a vital part of the accounting process of any organization. This policy indirectly emphasizes accurately preparing financial statements on time, which leads to timely tax filings and smooth audit facilitation.

Table of contents

Full Disclosure Principle Explained

The full disclosure principle is a process of reporting all important information related to the business in its financial statements in a clear and precise manner so that any user, be it the management or other stakeholders, can access it, understand it and use it to make important financial decisions.

The information includes not only the financial data related to the transactions done throughout the year, but also the audited statements, all the schedules and notes related to them, any risk in the business operations or future decisions, and a guidance for the management.

It also helps creditors, debtors, and other stakeholders have a clear view of the organization's financial health. The disclosure also makes it easier for the ordinary public to understand the books of accounts and decide whether to invest or not in an organization. We can consider that the full disclosure principle inculcates overall faith in the organization, which is also good for the economy and country in the long run

The full disclosure principle accounting also helps creditors, debtors, and other stakeholders have a clear view of the organization’s financial health. The disclosure also makes it easier for the ordinary public to understand the books of accounts and decide whether to invest or not in an organization. We can consider that the full disclosure principle inculcates overall faith in the organization, which is also good for the economy and country in the long run.

It ensures transparency and provides necessary details to everyone. Such information, be it supplementary or data displayed in the financial statements, all are equally important. It not only indicates the current financial position but also reveals any ongoing legal proceedings, potential liabilities or the various methods and rules being followed by the business.

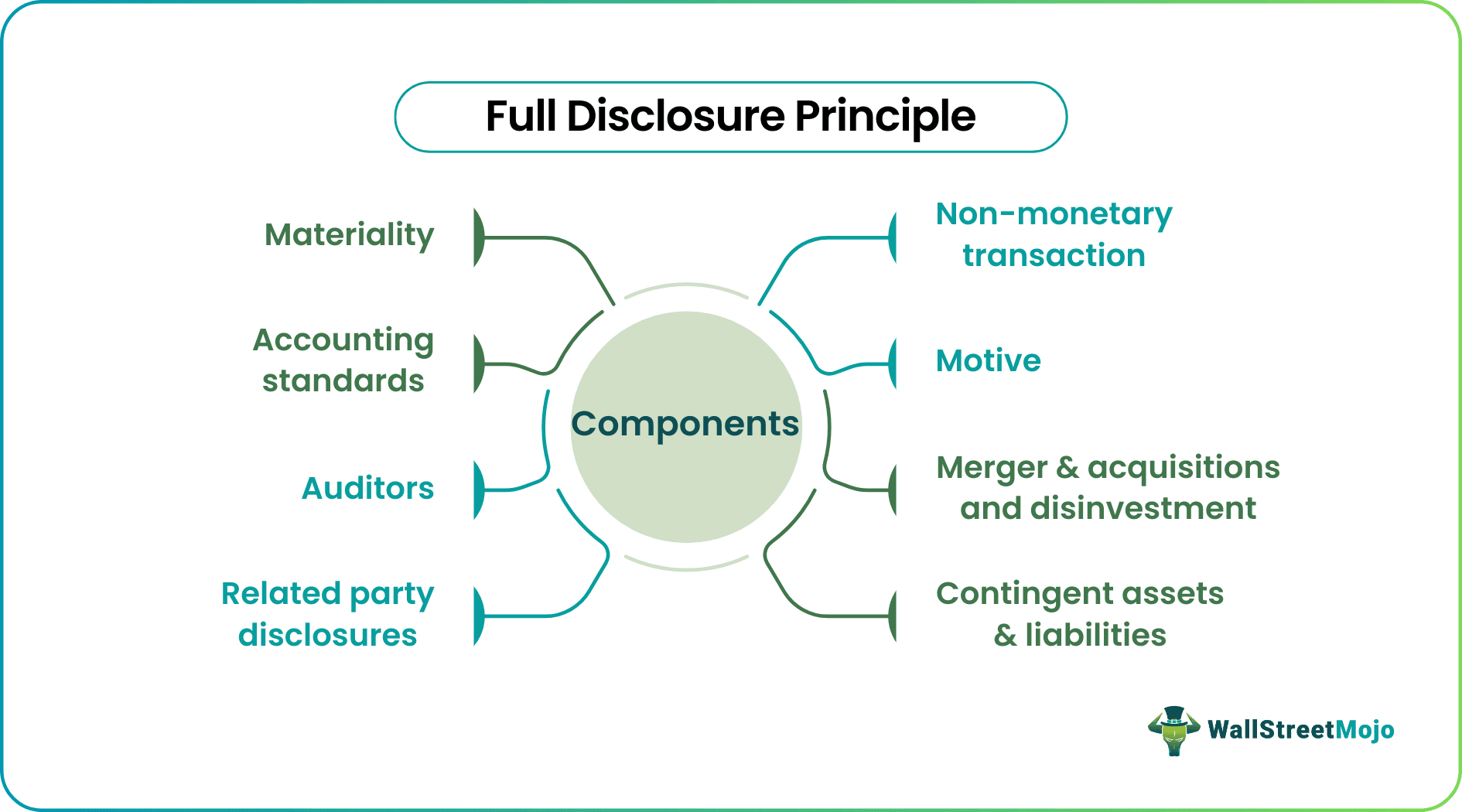

Components

Below is the list of components which are as follows:

#1 - Materiality

A material item is something that is significant and impacts the decision-making process of any person. When an organization prepares its financial statements, it should ensure that every little detail relevant to any party is included in the books of accounts. If you cannot include it in the financial reports, it must be shown as a footnote after the reports.

#2 - Accounting Standards

Accounting standards in every country are like traffic rules which everyone must abide by. The accounting standards make it compulsory to disclose the standards followed by an organization in the current year and past years. Also, any change in method or accounting policies from last year should be disclosed with the reason specified for the change. It will help the other party to understand the rationale behind the change.

#3 - Auditors

Auditors are one of the components of the full disclosure principle, which is also supposed to ensure that the company has disclosed every vital information in the books or footnotes. In case of any doubt, the auditor sends the confirmation query to any third party. Also, in cases where the auditors are not confident about in-house data, they must seek confirmation from higher management and senior leadership to ensure that numbers in the financial reports reflect credibility.

#4 - Related Party Disclosures

Suppose an organization does business with another entity or person defined by law as a related party. In that case, the former has to disclose it to auditors and in the books of accounts. Related party disclosure ensures that two entities don’t get involved in money laundering or reduce a product's cost/selling price.

#5 - Contingent Assets & Liabilities

Contingent assets and liabilities are those that expect to materialize shortly and the outcome of which depends on certain conditions. For example – if there is a lawsuit in process and the company expects to win it soon, it should declare this lawsuit and winning amount as contingent assets in the footnote. However, if the company expects to lose this lawsuit, it should declare it and win the amount as a contingent liability in the footnote.

#6 - Merger & Acquisitions and Disinvestment

Suppose the company has sold any of its products or business unit or acquired another business or another organization unit of the same business. In that case, it should disclose these transaction details in the books of accounts. Also, the details regarding how this will help the current business, in the long run, should be mentioned.

#7 - Non-Monetary Transaction

It’s not always that only the monetary transaction impacts the organization and other stakeholders. Sometimes change in the lending bank, appointment or release of an independent director, and change in the shareholding pattern is also material to the stakeholders in the organization. So, the organization should ensure that any of these activities are disclosed in the books of accounts.

#8 - Motive

The rationale behind the full disclosure principle is that the accountants and higher management of any organization do not get involved in malpractice, money laundering, or manipulation of books of accounts. Also, it will be easy to form an informed judgment and opinion about the organization when an outsider has full information about loans, creditors, debtors, directors, significant shareholders, etc.

Example

Let’s consider that X Ltd. has revenue of $5 Million and above in the last three years, and they have been paying late fees and penalties to the tune of $20,000 every year due to delays in filing annual return. If this $20,000 club has taxation fees, then not many people will know that this is not a tax expense but late fees and penalties. Simultaneously, if shown separately, an investor might question the organization's intent to file annual returns as there is a delay consistently in all three years. So as per the full disclosure principle, this $20,000 should be shown under late fees and penalties, clearly explaining the nature, which should be easily understandable to any person.

Advantages

Let us go through the advantages of the full disclosure principle accounting in details.

- It makes it easier to understand financial statements and form a decision;

- It makes the usage and comparison of financial statements easier.

- Improves the goodwill and integrity of the organization in the market;

- Inculcates best practices in the industry and improves public faith in the organization;

- Essential for audits and applying for loans.

Disadvantages

Some disadvantages of the process are as given below:

- Sometimes inside information disclosed outside might be harmful to the company.

- Competitors might use the data against the company, which will be bad for business.

- Since a lot of important information is revealed in the financial disclosures, there may be an overload of information and the users may not understand which is relevant to the requirements. Thus, there is complexity of the data.

- From the above point is can be concluded that user who may not be having good knowledge about the methods of interpreting the details, may find it difficult to understand them and use them to their advantage.

- Preparing such detailed statements will not only be tiem consuming but there is also room for errors. So utmost care and caution is necessary while preparing them.

Thus, the above are some noteworthy advantages and disadvantages of the concept. It is necessary to understand them so that the information can be applied properly for financial decision making.

Points to Note about Changes in Full Disclosure Principle

Nowadays, with the development of the accounting system, it is easy and quick to prepare the books of accounts as all the departments are interlinked through ERP – Enterprise Resource Planning systems. It also makes the disclosure easier as most of the information is readily available from computers. Also, the accountants must ensure to implement any change in the tax rate, reporting format, or any other change before disclosure is made.

Recommended Articles

This has been a guide to what is Full Disclosure Principle. We explain it with example, components, advantages and disadvantages. You can learn more about accounting from the following articles –