Table Of Contents

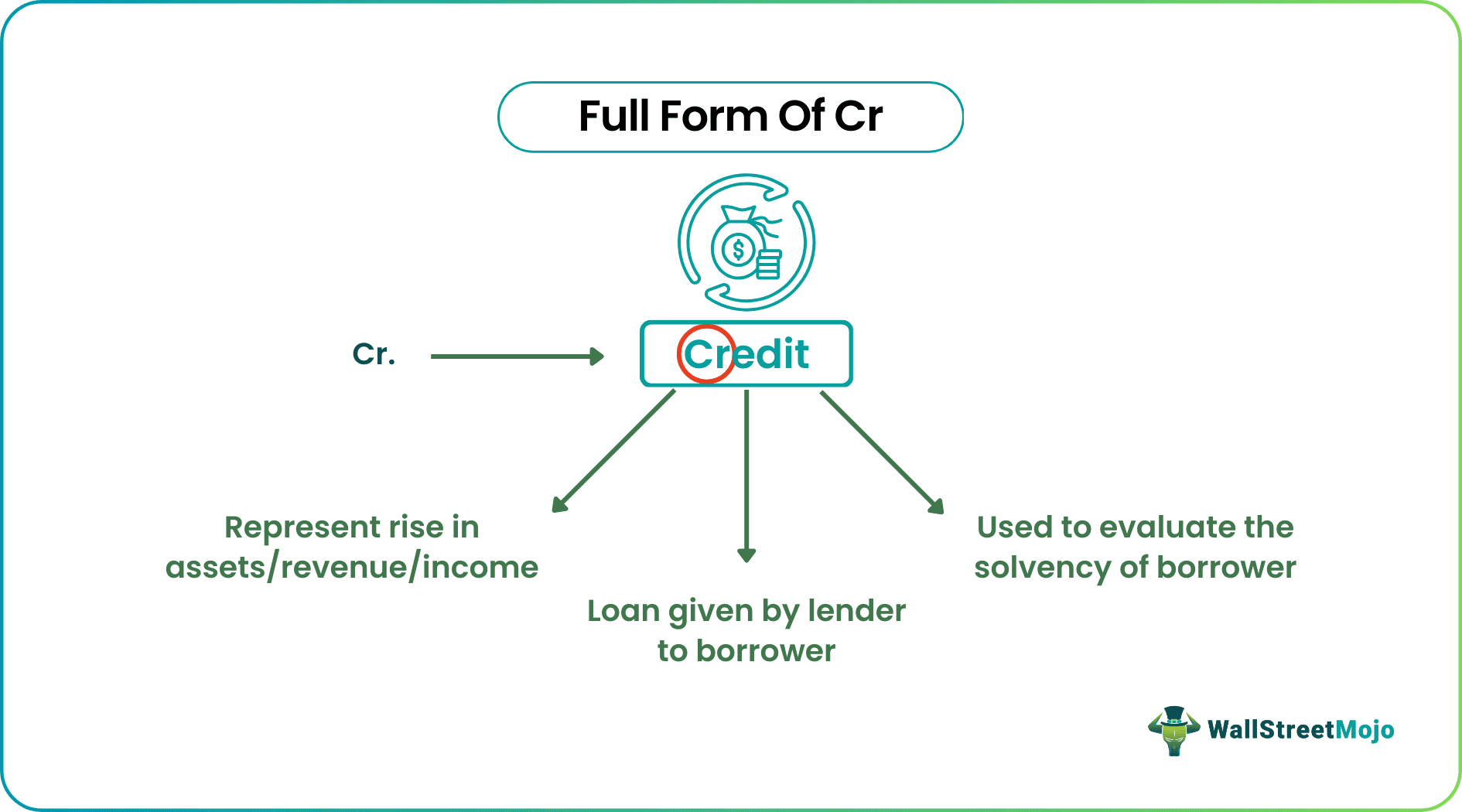

What Is The Full Form Of Cr - Credit

The full form of CR is Credit. The word credit has different meanings in the world of financial accounting as sometimes it can be referred to as a journal entry made on the right-hand side of an account representing a rise in assets and records all the income and revenues (in nominal accounts), what goes out (in real accounts) and is regarded as a giver (in personal accounts).

It also represents an agreement between a borrower and a lender concerning the loan amount borrowed by the former from the latter for a particular period. Credit refers to a journal entry that is recorded on the right-hand side of a T ledger account. The characteristics of Credit or Cr are character, capacity, capital, collateral, and conditions. Credit has its advantages and disadvantages.

Table of contents

- What Is The Full Form Of Cr - Credit

- Cr stands for Credit in accounting. It represents increased assets, records income and expenses, and acts as an account giver. It can also refer to a borrowing agreement between a lender and a borrower.

- There are different types of Credit, including financial and bank loans such as mortgages, home loans, car loans, educational loans, signature loans, business loans, and credit lines.

- Credit is recorded on the right-hand side of a T ledger account as a journal entry. The features of Credit, also known as Cr, include character, capacity, capital, collateral, and conditions.

Full Form Of Cr Explained

The full form of cr is credit, which is normally used in a variety of context in the financial market. It not only represents the credit side of accounting in the ledger, which records sales, income, capital account, gains, liabilities, etc, but it also tells us about the funds that a lender extends to the borrower with the expectation that the borrower will repay it in future.

When the borrower gets credit from banks or any other financial institutions, it is because they do not possess it and need it for urgent purpose which may be some purchase, investments or any other financial obligation.

A borrower must self-evaluate whether they are ready or whether they must borrow a loan to fulfill a specific purpose. A borrower must look at both the advantages and disadvantages of taking credit and then self-assess himself and his purpose behind making such a decision to make the best use of his decision and not have to regret in the future.

It is essential to understand the full form of Cr in bank because credit is a very important component in the financial system. It helps in making the money move and earn return through proper and beneficial investment opportunities. It is very difficult for businesses or individuals to always have ready funds to meet their obligations. In such situations credit provides the money necessary to handle the situation. Thus it helps in growth, expansion, investment, purchases and many other financial activities that are a part of an economy.

Characteristics

The five characteristics of credit are discussed as follows-

- Character - Their credit history can determine the borrower's character. Character is the foremost characteristic of Cr or credit and is also regarded as credit history. The applicant can justify their character by proving themselves as a responsible borrower. Determining an applicant's character is crucial for lenders to protect themselves from defaulting customers.

- Capacity - The capacity of a loan application can be determined by its debt to income ratio. Determining a borrower's capacity is crucial for the lenders to confirm his ability to repay the loan.

- Capital - The capital signifies a borrower's total funds and resources. Capital can be determined by the amount of money a loan applicant has invested in his business. The greater the contribution, the greater the chances for him or her to qualify for the loan.

- Collateral - Collateral signifies the security the borrower has pledged against the loan they have applied for. Collateral security acts as a backup if the borrower cannot repay the loan amount in the future.

- Conditions - Conditions signify the amount involved, the real purpose of applying for the loan, and ongoing interest rates.

Types

The full form of Cr in bank is credit that can be of various forms. It can be in the form of financial credit or bank loans, which includes mortgages, home loans, car loans, educational loans, signature loans, business loans, and other credit lines. There are other forms of credit too. For example, the exchange of products or services against deferred payment, the credit offered by the suppliers or creditors to the company against the number of raw materials purchased by the latter, etc. Let us elaborate them:

- Loans – Borrowers get loans from banks and financial institutions for different purposes which are termed as credit in the financial market. Loans can be of different types, like mortgage related loans, educational loans, business loans, etc. The amount varies as per the nature or the purpose for which they are taken. As per the terms of the contract the loans are extended based on repayment of an interest whose rate depends on the market rates. They may also change depending on market fluctuations. The lender gives loans with the expectation of getting the principle along with interest back from the borrower after a certain period of time.

- Credit Cards – Credit cards are a form of facility that are given to customers of banks and financial institutions. Customers can use these cards to make payments on credit related to online purchases, which can be paid through installments on a monthly basis along with interest. Credit card holders can also take loans against them upto a certain amount. the credit limit is set by the issuer of the card, depending on the borrower’s credit history.

- Lines of credit – This is also another type of facility that borrowers can access, in which they can withdraw a certain predetermined amount of money from the bank as and when they need. The interest is charged on the amount withdrawn. The terms and conditions of repayment may vary.

- Trade Credit – Very often business extend credut facility to one another. The supplier may sell goods to customers and accept payment terms on credit. The purchaser or customer gets the facility to make payment after a certain period of time but within the due date. This credit period is beneficial to purchases as they can arrange for funds and there is no immediate cash outflow.

Thus, the above are different types of credit available in the market, each of which have their own pros and cons. It is necessary for the borrower to understand and evaluate their capacity before taking loans. Similarly lenders should also assess the creditworthiness of borrower before extending loans.

Examples

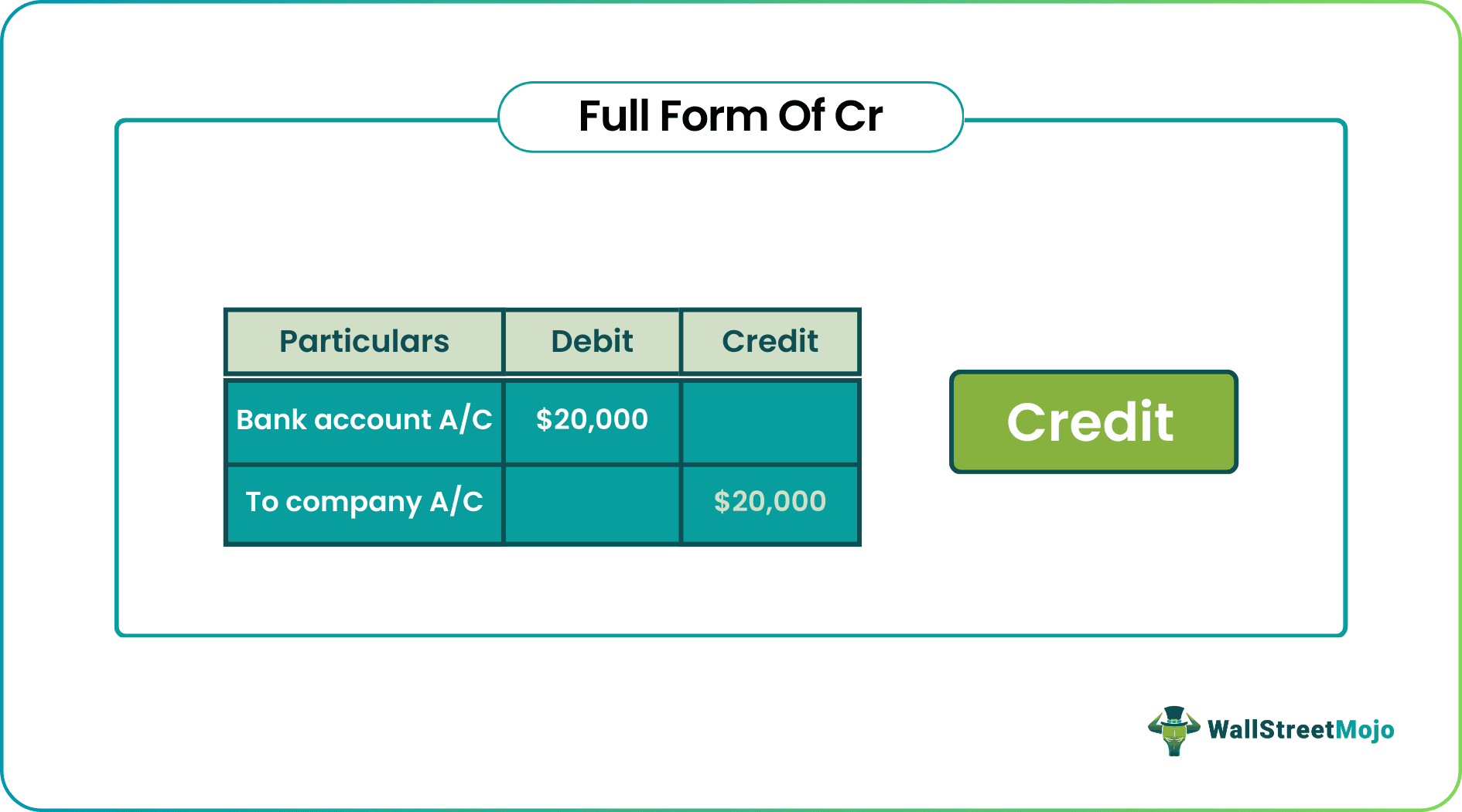

Now Let us try to understand the concept with the help of a suitable example.

ABC Limited took a loan of $20,000. The company has an underlying credit of $10,000 and a debit of $200. The carrying balance of the company is $9,800 ($10,000-$200). This means ABC owes $9,800 to its creditors. The credit balance at the end of that year would be $29,800 ($20,000+$9,800).

Advantages

The advantages of credit are discussed as follows-

- Credit gives the borrowers the option to buy something even if they lack sufficient funds for making such a transaction in the present and enables them to repay the loan amount over time, all at once or in EMIs (monthly installments).

- The credit option makes it easier for borrowers to buy what they want at their own pace without worrying about the available funds.

- Credit options from a banking or financial institution reduce the borrowers' burden to pay the full amount in one shot. The borrowers can make a down payment and avail the option of paying monthly EMIs spread over some time.

Disadvantages

The disadvantages of credit are as follows-

- The borrowers will be required to pay interest on the loan.

- The borrowers will be required to pay late fees if they default a payment.

- The borrowers can even impact their creditworthiness if they default on their loan payments.

- Impacted credit rating will make it difficult for borrowers to secure a loan or credit in the future.

Being able to identify the advantages and disadvantages of a financial concept is important because it becomes possible to implement them for appropriate purpose. Both borrowers and lenders should keep the pros and cons of credit facility in mind before entering into a contractual obligation to extend and accept funds so that the resource becomes useful for both the parties.

Credit Vs Debit

Both the above financial terms are widely used to describe the matters related to any kind of transaction. However, it is important to understand the differences. The difference between credit and debit are discussed as follows-

- Definition - Debit is recorded when there is a rise in the value of assets, losses, dividends, expenses, or fall in the value of liabilities and shareholders' equity. On the other hand, credit can be defined as a journal entry that is recorded when there is a fall in the value of assets or a rise in the value of incomes, gains, revenues, liabilities, and shareholders’ equity.

- Treatment in personal accounts - In a personal account, debit is regarded as the “receiver,” while credit is regarded as the “giver.”

- Treatment in real accounts - In a real account, debit is regarded as what “comes in,” while credit is regarded as what “goes out.”

- Treatment in nominal accounts - In a nominal account, all expenses and losses incurred by an organization are "debited" while all incomes and revenues are "credited."

- Left/ right side in a T-format ledger - A debit entry is recorded on the “left-hand side” in a T-format ledger. On the other hand, a credit entry is recorded on the “right-hand side” in a T-format ledger.

- Use - Debit generally indicates an increase, whereas credit depicts the amount withdrawn.

Frequently Asked Questions (FAQs)

"Credit sales" is when a customer receives goods or services but pays for them later rather than immediately at the time of purchase. It means the customer only makes a partial payment during the purchase.

When recording financial information, a debit is made on the left side of an account, while a credit is made on the right side. It leads to a corresponding increase or decrease on either side of the report.

When there is an increase in liabilities or shareholders' equity, it is recorded as a credit in the account and is indicated by the abbreviation "CR." Conversely, a decrease in liabilities is registered as a debit and is indicated by the acronym "DR."

Recommended Articles

This has been a guide to what is Full Form Of Cr. We explain its characteristics and types with example, advantages, disadvantages & differences with debit. You may refer to the following articles to learn more about finance –