Part of our Accounts Payable & Receivable guide

What Is Advance To Employee?

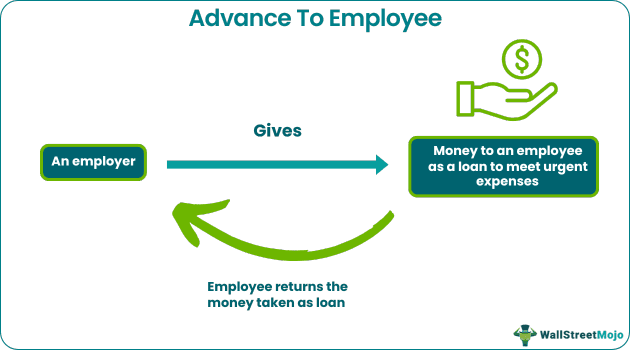

An Advance to Employee is a stopgap financial arrangement for employees, where an employer extends it as a loan to help an employee meet personal or professional expenditures. It is recorded as an asset (advances or loans) in the company’s books of accounts since the employee is expected to repay the loan.

Employers may extend these loans to help staff members meet work-related travel expenses, personal emergencies, etc. They may also be given to facilitate employee relocation. Such loans may be required during payroll transitions as employees may need funds for personal expenditure until the next payday. The repayment terms are defined and communicated to the employee when the loan is given.

- An Advance to Employee is a short-term loan extended by an employer to enable the employee to meet urgent expenses. Employees must repay these loans.

- These advances may be given to help employees cover work-related expenses, urgent personal expenses, or relocation expenses.

- Employees may also use such advances to make temporary financial arrangements during payroll transitions or irregularities.

- Making the right accounting entries is essential from the perspective of good management and accounting compliance. It is advisable to monitor the frequency of such requests from employees to ensure hassle-free operations.

Advance To Employee Explained

An Advance to Employee is a short-term loan an employer gives their employee to help them meet urgent personal or professional financial needs. These loans are extended with the expectation that they will be repaid within a set timeframe. Since these loans impact a company’s cash flows, they are recorded in the books of accounts and subsequently show up in its financial statements. Any potential tax implications must be considered both by employees and employers while entering into such loan agreements.

This explanation seems incomplete without the mention of a key aspect, which states how advance to employee differs from salary advance. A salary advance involves getting a portion of the salary or the full salary as an advance in times of need. However, in case of an advance to employee, the amount is treated as an asset in the company’s books. Hence, it is not part of an employer’s financial obligation or commitment to an employee. It is an independent provision of funds made specifically for employees per their request.

To secure this advance, employees submit a request to their employers. They may be required to take eligibility criteria into account before doing so. For instance, some companies may extend advances only to those who have completed a specific duration or tenure with them. Once the request is sent to the relevant team or authority, it is reviewed and processed within a specific period. The decision-makers may approve or reject such requests at this stage. The frequency of such requests must be given due consideration while approving them to ensure employees do not exploit this facility.

If the request is approved, an agreement is finalized and signed, where repayment terms are mentioned. Based on this, the amount is released. Employees are expected to repay in line with the terms and conditions of the agreement. At times, employees may not make sincere efforts to repay such advances, or they may exhibit dissatisfaction in various ways when an employer deducts the loan amount from their paychecks. Hence, it is important to review loan requests carefully to avoid these problems.

From a human resource perspective, cash advances to employees can help build trust between employers and staff members. They effectively solve employee problems related to unexpected expenses and urgent financial needs. Such facilities also improve employee engagement and retention levels as employees can avoid securing funds from other sources where interest rates may be high.

Examples

Let us study a few examples to understand the topic in detail.

Example #1

Suppose Emily is employed at CDF Corp. in Texas. She plans to buy a car and needs money for a down payment. As the car company she chose was running certain attractive offers, capitalizing upon this deal early was crucial. Hence, Emily submitted a loan request to meet this expenditure.

When the request was approved, she received $3,000 from her employer. Per the terms of the advance to employee contract, Emily was required to repay the loan in the next 3 months. The financial assistance Emily received from her company enabled her to purchase the car, taking advantage of specific promotional offers. Her employer deducted the loan amount in the next 3 months and recovered the entire amount.

Example #2

Steffany, a sales representative at Lunar Gene Pharmaceuticals, is scheduled to attend a conference in California. Her company assigned her the responsibility of attending this conference to build professional relationships and secure contacts in the region. She needs around $5,500 to meet all conference-related expenses, including registration, travel, and accommodation.

The accounting department at Lunar Gene Pharmaceuticals gave her the money needed to meet these expenses as an advance. Steffany attended the conference, and upon returning from California, she submitted all the relevant bills, registration documents, and flight tickets. The accounting department matched the bills with the expenses she quoted and adjusted the advance to employee account accordingly.

In this way, Steffany was able to attend the conference, fulfilling her responsibilities as a sales representative at Lunar Gene Pharmaceuticals without dealing with the burden of raising funds independently for her company trip.

How To Record?

Advance to Employee has legal and financial implications for a company. Hence, it is important to record these advances in the stipulated manner. Companies make advance to employee journal entries in line with the standard accounting practices. It is pivotal to understand the advance to employee accounting entries to record these transactions correctly.

- Advances are recorded as assets in a company’s balance sheet.

- Per company policy or industry practices, such assets are categorized under the account called Employee Loans or Advances.

- The company’s bank or cash account is credited (decreased) and the employee advance account is debited (increased).

- The advance repayment entry is made by crediting the employee’s advance account and debiting the company’s bank or cash account.

- One must bear in mind that these are post-tax deductions.

Journal entry for advance extended to an employee:

| Date | Account Titles/Particulars | Debit ($) | Credit ($) |

|---|---|---|---|

| 1 Jan 2024 | Employee Advance Bank | $$$ | $$$ |

Journal entry for repayment made by an employee:

| Date | Account Titles/Particulars | Debit ($) | Credit ($) |

|---|---|---|---|

| 1 Mar 2024 | Bank Employee Advance | $$$ | $$$ |

Employee advances must be formally recorded, and the contracts must be retained for future reference. Using accounting software, accounting teams must track repayments and close these accounts once employees repay the entire amount.

It is important to note the nature of such requests to ensure reasonableness in dealings. Also, once an advance is approved and processed, the accounting department must monitor the account to confirm whether repayment is on schedule.

Frequently Asked Questions (FAQs)

1.Why is advance to employees a financial asset?

Advances to employees are treated as assets in the company’s books of accounts because these amounts are short-term loans extended to employees. Money employees receive from employers in this manner must be repaid per the terms of the agreement.

2.Is advance to employees the same as payroll advance?

A payroll or paycheck advance is not the same as advance to an employee. Employee advances are loans given by employers for personal or professional financial needs. A payroll advance involves paying an employee’s salary in advance to help them meet personal emergencies or other financial needs.

3.Is advance to employees a prepaid expense?

Prepaid expenses refer to assets whose value has not yet been realized. For instance, rent and insurance, when prepaid, become assets because the benefit will be realized in the future. Advances given to employees can be categorized as prepaid expenses only in situations where the funds are given to an employee who is expected to bear certain expenses on behalf of the company. For example, if an employee is out on an official tour, the company may give the employee money to cover travel expenses in advance.

Recommended Articles

This article has been a guide to what is Advance to Employee. Here, we explain the concept in detail with how to record it and its examples. You may also find some useful articles here –

Recommended Articles

Continue with these closely related articles from the same guide.