Part of our Accounts Payable & Receivable guide

Credit Note Meaning

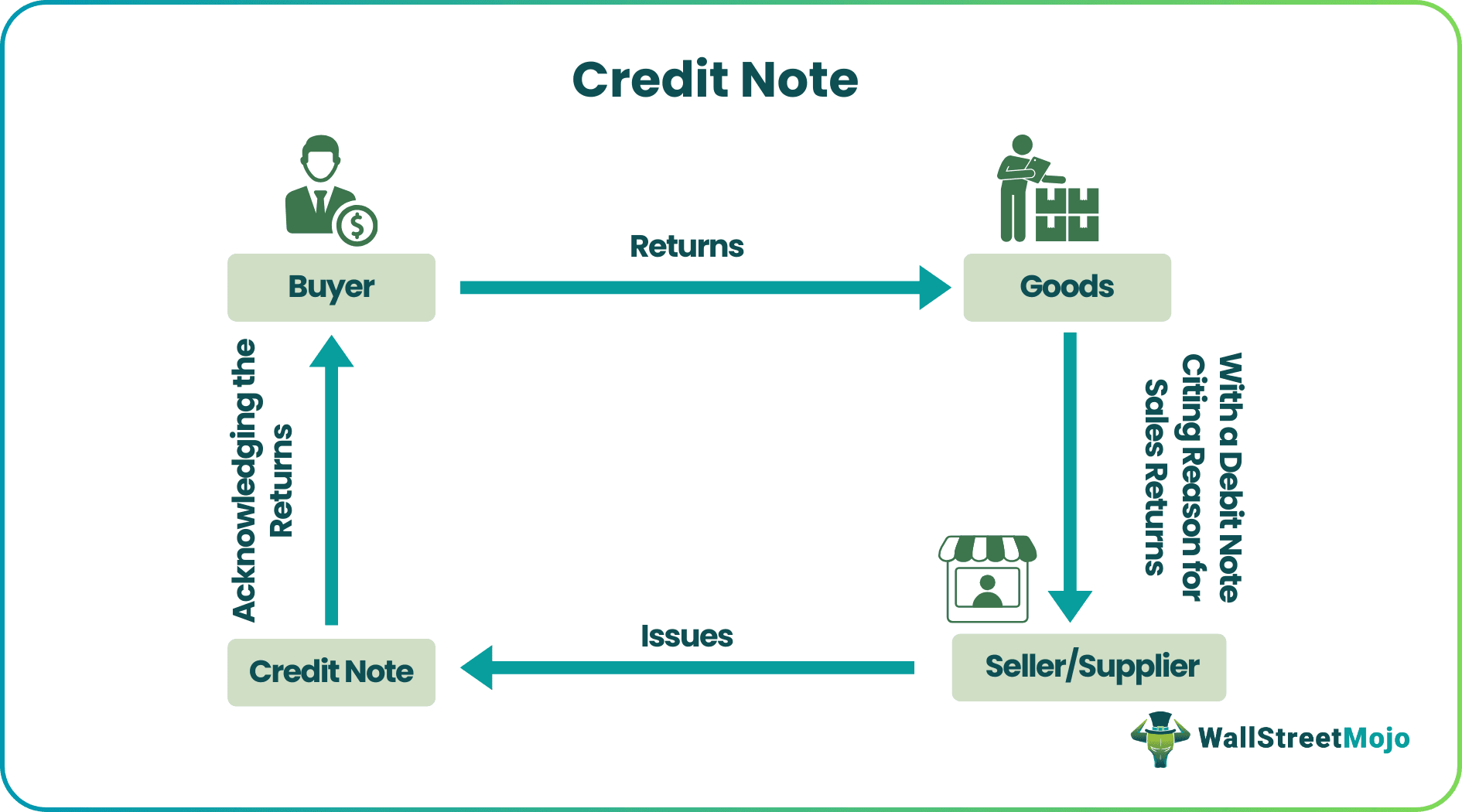

A credit note is a financial document that sellers provide to buyers as a token of confirmation against registered returns. It acknowledges the cancellation and lets the sellers make a credit entry to the buyers’ account for the required amount. Besides, it records the returned goods as return inwards for further processing or adjustment of the balance.

Also referred to as credit memos, these are issued after the invoices are prepared. However, there is a need to cancel either all or part of the orders returned in the process. Furthermore, this entry indicates crediting the buyers’ account in the accounts book of the sellers.

- A credit note is a commercial document issued by sellers to buyers to confirm sales returns.

- The amount that buyers are liable to pay is either less than or equal to the cost of the order.

- The credit memos are recorded in red ink to indicate a liability or reduced sales on the supplier or seller side.

- Buyers can also issue these notes if they are undercharged or paid less than the invoiced amount.

How Do Credit Notes Work?

A credit note is a commercial instrument that sellers issue to purchasers whenever they return goods bought on credit. This note acknowledges and notifies the suppliers to update the accounts book accordingly. As soon as the buyer returns the items, the seller recognizes them with a receipt, which indicates the entry of the same on the credit side of the buyer’s account.

The entry of this amount into the purchasers’ record signifies a reduction in the amount payable by customers or buyers. This is because they already returned the items and are no more liable to pay for the same. If the due amount is zero at that point, the purchasers get an opportunity to adjust the cost of the returned items against the next purchase.

Credit Note Video Explanation

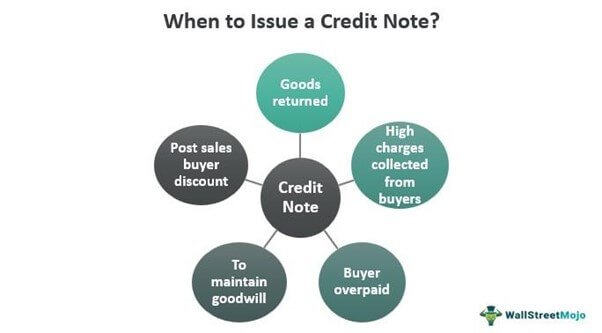

When To Issue Credit Notes?

As already stated, a party issues a credit memo when the other party cancels the order or returns an item, making suppliers or sellers record the same as a credit entry into the account books.

The purchasers might cancel or return all goods or only a part of the order. Here are a few other reasons to check when the credit note is issued:

- To maintain goodwill and the seller-buyer relationship remains strong and transparent

- Goods returned due to quality issues, defects, or service rejection

- Higher charges collected from buyers

- The buyer paid more than the amount invoiced

- After-sales buyer discount

- The customer received an amount lower than the invoiced amount.

Example – Credit Note Accounting

Company A buys goods worth $20,000 from Amazon but finds that 1% of them do not meet the quality standards. So, the company issues a debit note stating the same. So, let us check what Amazon’s journal entry in the books of accounts looks like.

The journal entry signifying a credit note format looks like –

| Sales A/C …….Dr | 200 | |

| To Company A | 200 |

The full version of the credit note example in the form of journal entries made pre and post-issuance of this note:

| Company A A/C………Dr | 20,000 | |

| To Sales A/C | 20,000 | |

| Sales A/C………..Dr | 200 | |

| To CompanyA A/C | 200 | |

| Sales Return A/C………Dr | 200 | |

| To Sales A/C | 200 |

Features

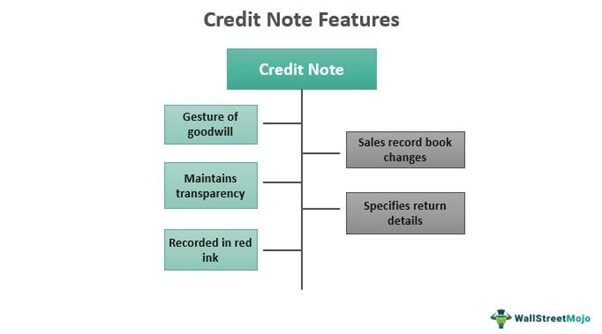

While sellers normally issue the credit memos to buyers against the returns they register, it might be a vice-versa scenario. The buyer can also issue a credit memo to sellers if undercharged or paid less than the invoiced amount.

Besides the point mentioned above, here are a few more traits that a credit memo exhibits:

- Suppliers/sellers record it in red ink to mark reduced sales and liability.

- A credit memo is a gesture of goodwill.

- The sales return book changes as per the reduced sales of defective goods

- A credit memo is an acknowledgment note that keeps the buyer-seller relationship transparent.

- It specifies the number of goods or items returned.

Credit Note vs Debit Note

A credit memo is a financial document provided to buyers to acknowledge their registered returns with the sellers or suppliers. This note signifies the acceptance of the sales returns. The customer account gets a credit entry, and the sales return becomes a debit entry in the supplier’s account.

On the other hand, a debit note is a document buyers provide to sellers to notify them of the returns and the reasons behind it. As a result, the supplier account is debited, and purchase returns are credited to the buyer’s accounts.

Let us explore an example to understand the difference between credit note and debit note:

Suppose a seller supplies goods to a buyer along with a tax invoice. Upon receiving the order, the buyer finds faults in the products and returns the same to the seller with a debit note. The supplier accepts the debit note and prepares a credit memo, handed over to the buyers as an acknowledgment. This is how it works.

Frequently Asked Questions (FAQs)

What is a credit note?

It is an acknowledgment instrument that sellers provide to buyers when they return all or a portion of an order. It notifies both sides of the reduced sales of the supplier or sellers and lets them know the amount the buyers are eligible to receive against the returns. Here, the customer/buyer account is credited, and the sales returns are debited in the supplier’s account.

When is a credit note issued?

It is issued in the following scenarios:

· Goods are returned due to quality or other issues

· To maintain the seller’s goodwill

· Buyers underpaid or overpaid

· Post-sales discount introduced, etc.

Is a credit note a refund?

A credit memo is not a refund or monetary exchange. Instead, it acts as a voucher that could be used to adjust or balance the required amount in future dealings or invoices.

Recommended Articles

This article is a guide to Credit Note, its meaning & features. Here we explain how it works in accounting & when it is issued, along with a practical example. You can also learn about basic accounting from these articles below –