Table of Contents

What Is Recording Transaction?

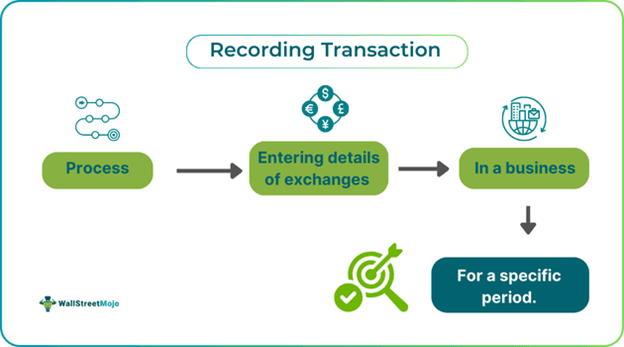

Recording transactions in accounting is a process where businesses enter transactions in journal books, cash books, ledger accounts, etc. The documents are proof of different transactions that took place in relation to the business in a specific period.

Recording all transactions in a business helps it assess its financial status. It helps the company understand whether it is making money, the details of debt owed, and the credit received. The records show if the company can meet its obligations and understand the value of the organization in the market.

Key Takeaways

- Recording transactions in accounting is a foundational step that records financial data in a business's books of account.

- Transactions are descriptions of exchanges between buyers and sellers. All transactions are analyzed by nature, and their impact on the business's finances is recorded accordingly.

- Types include journal entries, supplier invoice payments, and paychecks.

- The process involves identifying entries, segregating the information into ledgers, and preparing trial balances and their rectification. This forms the base for preparing financial statements.

- It helps track expenses and income, ensures compliance with standards, and provides an accurate and fair view of the business.

Recording Transactions In Accounting Explained

Recording transactions in accounting is considered the fundamental step in the accounting process, where all transaction details are entered into their respective books. Transactions are events or conditions that are recorded in the business books as they affect the business's financial condition. They are agreements made between buyers and sellers based on the items (goods or services) transferred. They are a business occurrence that has monetary effects on the company's financial records.

Exchanges in a business are determined based on their nature and what accounts they will affect. The second step is recording them in their specific accounts and into the debit and credit columns. They are then recorded in a document called a journal.

The recorded transactions are categorized and segregated into many types. They include ledger accounts, sales and sales returns books, purchase and purchase returns books, cash books, bills receivable and payable books, etc.

These records act as evidence of business dealings that have taken place. They provide necessary information like the date, place, time, and amount involved in the transaction. They help in future verification and can be used as proof in a court of law when needed.

Process

The process of recording transactions involves the following steps:

- The first step is to analyze the nature of each transaction and assess the impact it creates on various accounts.

- The second step is to record the transaction in a double-entry bookkeeping journal.

- The information entered in the journal is then segregated and recorded in the respective ledger accounts.

- The next step is to prepare a trial balance, which shows the errors incurred while recording the accounts.

- The next step shall be to make necessary entry adjustments.

- Once the trial balance is prepared after proper checking, the next step is to proceed with the profit and loss account, income statement, balance sheet, and other financial statements.

Types

Given below are some of the types of transactions recorded:

- Journal entries - It is the basis of entering information in the books of accounts. The numbers, debit, and credit details of all transactions are entered.

- Receipt and issuance of supplier invoices - On receipt of the invoices, the transactions are entered accordingly. For instance, the debits the expenses and credit accounts payable. Similarly, the invoice numbers are entered when the suppliers are paid. Cash is debited, and the accounts receivable account is created when the sales account is credited.

- Issuance of suppliers' payment - When suppliers are paid, the invoice numbers are recorded in the accounts payable section. Debiting and crediting of accounts payable and cash accounts are also done successively.

- Paychecks - Pay rates and hours worked are recorded, and compensation is debited along with payroll tax expense accounts. Cash is then credited where deductions are necessary.

Examples

Let us look at some of the examples to understand the concept better.

Example #1

Suppose Dan is a business owner of a small garment shop. He has a ledger book where he writes down all of his daily transactions. Every day, he records all of the transactions, regardless of whether they are big or small. This helps in calculating the expenses he has incurred in running the business and if they are sufficient to make a living. To understand his finances, Dan subtracts all his expenses from the income he receives and checks with the investor to ensure accuracy. By analyzing and recording transactions, Dan effectively manages his finances and stays informed about his financial health.

Example #2

An article published on June 24, 2020, claims that German payment processor Wirecard AG fraudulently claimed €1.9 billion in cash held in trustee accounts in the Philippines, which never happened. According to an external audit, Wirecard had been creating fake transactions for years to conceal large debt and boost its financial position.

Due to this fraud, the company went bankrupt, important executives were arrested, and investors suffered significant losses. The controversy emphasizes recording transactions should be transparent to show a company's actual financial health.

Importance

Below are some of the points that highlight the importance of transaction recordings:

- Recording transactions in a journal of all exchanges helps the business keep track of its expenses.

- It helps businesses understand if they are making a profit.

- It helps businesses understand if there is a satisfactory or desired return on investment.

- It helps the business understand if the functions are aligned with their business's vision and mission. The records help cross-check deviations.

- It helps the company analyze if they can meet any financial obligations.

- Analyzing and recording transactions helps companies understand their true financial positions.

- They are the source of information that is used for the preparation of balance sheets and other financial statements.

- They help in assessing the true and fair view of a company.

- It helps in easy audit.