Table of Contents

What Is Regulation G?

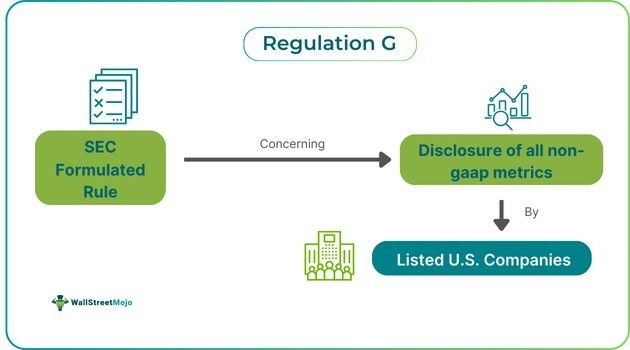

Regulation G refers to the SEC's established rule that governs the mandatory release of non-GAAP financial metrics by publicly listed US companies. These statements are not presented or calculated according to GAAP. The regulation serves to increase transparency by necessitating reconciliation of non-GAAP metrics to closely similar GAAP figures.

It ensures that accurate information reaches investors so they can make correct decisions. It has successfully promoted market confidence and integrity. It has applications in public reports covering earnings presentations and releases to foster accountability within financial accounting practices. Firms must exclude misleading representation to define non-GAAP metrics inside communications clearly.

Key Takeaways

- Regulation G is the SEC rule mandating that publicly listed US companies release non-GAAP financial metrics to enhance transparency by reconciling them with closely similar GAAP metrics.

- It covers public disclosure of non-GAAP finance metrics, enabling investor access, but excludes real estate loans, credit extensions, and certain business combinations.

- It applies to all public disclosures of non-GAAP financial metrics, mandating adherence to investor presentations and earnings releases, labeling non-GAAP measures, and monitoring adherence for investor protection.

- It applies to all public disclosures related to non-GAAP metrics, while Item 10(E) applies to all SEC filings.

Regulation G Explained

Regulation G, set up by the SEC in 2003, forces publicly listed firms to release non-GAAP financial metrics. These disclosures must reconcile to the closely similar comparable GAAP metrics, allowing investors to obtain accurate financial details.

SEC Regulation G must be applied to every public disclosure of material details involving non-GAAP measures. Firms must disclose the most directly contrastable GAAP metrics along with a quantitative reconciliation. As a result, it prevents any ambiguous and misguiding reflection of a company's financial performance.

The regulation aims to enhance openness and accountability within companies' financial reporting. The SEC has helped mitigate the risk of firms showing only positive financial results that might misguide investors and stakeholders into making wrong decisions.

Such crucial regulation has been used to transmit financial performance out of traditional GAAP measures. Hence, it often helps to underscore the firm's cash flow and operational efficiency. Nevertheless, all businesses have to comply strictly with guidelines to every letter and spirit to bring clarity and bypass any possible legal suit.

The financial landscape has positively impacted the manner in which companies display their financial results to stakeholders. As a result, it supports and strengthens the culture of commendable transparency in company dealings. Therefore, firms have been able to make highly informed investment decisions and amplified investor confidence regarding company public disclosures.

In short, the regulation has helped bring transparency and accountability to companies' public reporting, benefiting both companies and investors.

What Does And Does Not It Cover?

The regulation has the objective to standardize non-GAAP reporting while using and removing particular elements as follows:

Areas it covers:

- It includes public disclosure of non-GAAP metrics of finance mandating reconciliation to very closely comparable GAAP measures.

- It can be applied to all material information published, entailing non-GAAP measures to enable complete financial data access to investors.

Areas it excludes:

- It excludes individual loans collaterally secured by real estate.

- It can not be applied to credit extension to farms, businesses or individuals.

- It excludes those non-GAAP metrics that relate to planned business combinations regulated by certain communication laws.

- It also exempts foreign private issues under specific conditions while publishing non-GAAP measures beyond the borders of the US.

How Does It Apply?

It applies in the following manner:

- It has been applied to every public release or disclosure of material information concerning non-GAAP financial metrics, withier in writing or orally.

- It requires companies under the law to show the most closely comparable GAAP measure and all non-GAAP financial metrics published.

- A detailed quantitative reconciliation of non-GAAP and GAAP metrics should be reported for investors' clarity.

- It presents any willful omission or misguiding representation of non-GAAP metrics, creating an illusion about a company's financial performance in front of investors.

- As per the Securities Exchange Act of 1934, all companies besides registered investment firms fall under the regulation requiring them to file necessary reports.

- It mandates adherence to public disclosures on or after 28 March 2003, entailing investor presentation and earnings release.

- Excepting a few foreign entities, all foreign and domestic companies have to comply with the regulation of G.

- All public companies have to label and describe all non-GAAP measures in their reports to avoid any confusion related to calculation and nature in investors' minds.

- SEC continuously monitors the adherence to the regulation of G to protect the investors against potentially fraudulent financial disclosures.

Regulation G Vs. Item 10(E)

Both regulate the usage of non-GAAP financial metrics. But they have differences in terms of enforcement mechanisms, scope and requirements, as shown in the table below:

| Regulation G | Item 10(E) |

|---|---|

| Has application in all public disclosures related to non-GAAP metrics. | Has application in all SEC filings. |

| Mandates reconciliation and disclosure of GAAP to non-GAAP measures. | Needs extra restrictions and disclosures for SEC filings. |

| Has no requirement of specific prominence. | Has to present GAAP metrics with equitable or greater prominence. |

| It covers public disclosures and SEC filings both. | It has relations to particular documents of the SEC only. |

| It contains contained exclusions for financial measures under non-GAAP. | It restricts the exclusion of charges of cash settlement from non-GAAP measures pertaining to liquidity. |

| It needs the reconciliation to the GAAP measures that are most closely the same. | Has a similar requirement of reconciliation as that of its comparison element. |

| Various regulations of the SEC enforce it. | SEC stringently monitors adherence to it to prevent misguiding disclosures to users and investors. |