Part of our Equity Research guide

Equity Research Interview Questions

If you are called for an equity research interview, you can be asked any question from anywhere. However, you should not take this lightly as this can change your Finance career. Equity Research interview questions are a mix of technical and tricky questions. So, you need to have a thorough knowledge of financial analysis, valuation, financial modeling, the stock market, current events, and stress interview questions.

Let’s find below the top 20 Equity Research interview questions that are repeatedly asked for the positions of equity research analysts.

Question #1 – Do you know the difference between equity and enterprise values? How are they different?

This is a simple conceptual equity research interview question, and you need first to mention the definition of enterprise value and equity value and then tell the differences between them.

Enterprise value can be expressed as follows –

- Enterprise Value = Market Value of Common Stock + Market Value of Preferred Stock + Market Value of Debt + Minority Interest – Cash & Investments.

Whereas, the equity value formula can be expressed as follows –

- Equity Value = Market Capitalization + Stock Options + Value of equity issued from convertible securities – Proceeds from converting convertible securities.

The basic difference between enterprise value and equity value is enterprise value helps investors get a complete picture of a company’s current financial affairs. In contrast, equity value helps them shape future decisions.

Question # 2- What are the most common ratios used to analyze a company?

It can be classified as the most common equity research interview question. Here is the list of common ratios for financial analysis that can be divided into seven parts –

#2 – Turnover Ratios

- Receivables Turnover

- Days Receivables

- Inventory Turnover

- Days Inventory

- Accounts Payable Turnover

- Days Payable

- Cash Conversion Cycle

#3 – Operating Efficiency Ratio Analysis

- Asset Turnover Ratio

- Net Fixed Asset Turnover

- Equity Turnover

#4 – Operating Profitability Ratio Analysis

- Gross Profit Margin

- Operating Profit Margin

- Net Margin

- Return on Total Assets

- Return on Equity

- Dupont ROE

#5 – Business Risk

- Operating Leverage

- Financial Leverage

- Total Leverage

#6 – Financial Risk

#7 – External Liquidity Risk

Question #3 What is Financial Modeling, and how is it useful in Equity Research?

- This is again one of the most common equity research interview questions. Financial modeling is nothing but projecting the company’s finances in a very organized manner. As the companies that you evaluate only provide historical financial statements, this financial model helps equity analysts understand the fundamentals of the company – ratios, debt, earnings per share, and other important valuation parameters.

- In financial modeling, you forecast the company’s balance sheet, cash flows, and income statement for the future years.

- You may refer to examples like the Box IPO Financial Model and Alibaba Financial Model to understand more about Financial Modeling.

Question #4 – How do you do a Discounted Cash Flow analysis in Equity Research?

If you are new to the valuation model, please go through this Free training on Financial Modeling.

- Financial modeling starts with populating the company’s historical financial statements in a standard format.

- After that, we project these three statements using a step-by-step financial modeling technique.

- The three statements are supported by other schedules like the Debt and Interest Schedule, Plant and Machinery & Depreciation Schedule, Working Capital, Shareholders Equity, Intangible and Amortization Schedules, etc.

- Once the forecast is done, you move to valuations of the firm using the DCF approach,

- Here you are required to calculate Free Cash Flow to Firm or Free Cash Flow to Equity and find the present value of these cash flows to find the fair valuation of the stock.

Question #5 – What is Free Cash Flow to a Firm?

This is a classic equity research interview question. Free cash flow to the firm is the excess cash that is generated after considering the working capital requirements and the cost associated with maintaining and renewing the fixed assets. The firm’s free cash flow goes to the debt holders and the equity holders.

Free Cash Flow to Firm or FCFF Calculation = EBIT x (1-tax rate) + Non Cash Charges + Changes in Working capital – Capital Expenditure

You can learn more about FCFF here.

Question #6 – What is Free Cash Flow to Equity?

Though this question is frequently asked in valuation interviews, this can be an expected equity research question. FCFE measures how much “cash” a firm can return to its shareholders and is calculated after taking care of the taxes, capital expenditure, and debt cash flows.

The FCFE model has certain limitations. For example, it is useful only in cases where the company’s leverage is not volatile and cannot be applied to companies with changing debt leverage.

FCFE Formula = Net Income + Depreciation & Amortization + Changes in WC + Capex + Net Borrowings

You can learn more about FCFE here.

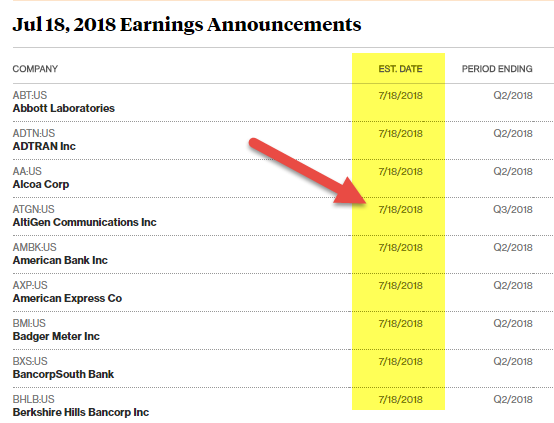

Question #7 – What’s the earning season? How would you define it?

Appearing for an equity research interview? – Be sure to know this equity research interview question.

source: Bloomberg.com

In our industry, companies will announce a specific date when they declare their quarterly or annual results. These companies will also offer a dial-in number using which we can discuss the results.

- One week before that specific date, the job is to update a spreadsheet, reflecting the analyst’s estimates and key metrics like EBITDA, EPS, Free Cash Flow, etc.

- On the day of the declaration, the job is to print the press release and swiftly summarize the key points.

You can refer to this article to learn more about the earning season.

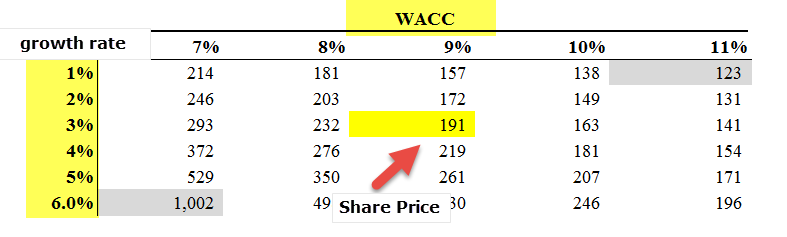

Question #8 – How do you do a Sensitivity Analysis in Equity Research?

One of the technology equity research interview questions.

- Sensitivity analysis using excel is one of the most important tasks after you have calculated the fair value of the stock.

- Generally, we use the base case assumptions of growth rates, WACC, and other inputs, which result in the base valuation of the firm.

- However, to provide the clients with a better understanding of the assumptions and their impact on valuations, you must prepare a sensitivity table.

- The sensitivity table is prepared using DATA TABLES in Excel.

- Sensitivity analysis is popularly done to measure the effect of changes in WACC and the company’s growth rate on Share Price.

- As we see above, in the base case assumption of a Growth rate of 3% and WACC of 9%, Alibaba’s Enterprise Value is $191 billion.

- However, when we can make our assumptions to say a 5% growth rate and WACC of 8%, we get the valuation of $350 billion!

Question #9 – What is the “restricted list,” and how does it affect your work?

This is a nontechnical equity research interview question. To ensure that there is no conflict of interest, a “restricted list” is being created.

When the investment banking team is working on closing a deal that our team has covered, we’re not allowed to share any reports with the clients, and we will not be able to share any estimates. Our team will also be restricted from sending any models and research reports to clients. We will also not be able to comment on the merits or demerits of the deal.

Question #10 – What are the most common multiples used in valuation?

Expect this expected equity research interview question. There are a few common multiples that are frequently used in valuation –

Question #11 – How do you find the Weighted Average Cost of Capital of a company?

WACC is commonly referred to as the Firm’s Cost of Capital. This is because the cost to the company for borrowing the capital is dictated by the external sources in the market and not by the company’s management. Its components are Debt, Common Equity, and Preferred Equity.

The formula of WACC = (Wd*Kd*(1-tax)) + (We*Ke) + (Wps*Kps).

where,

- Wd = Weight of Debt

- Kd = Cost of Debt

- tax – Tax Rate

- We = Weight of Equity

- Ke = Cost of Equity

- Wps = Weight of Preferred Shares

- Kps = Cost of Preferred Shares

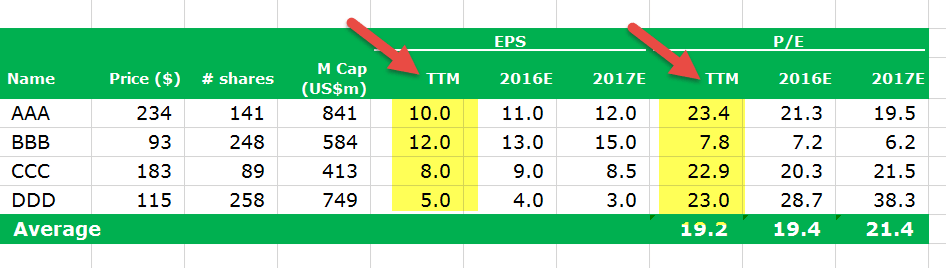

Question #12 – What is the difference between Trailing PE and Forward PE?

Trailing PE Ratio is calculated using the earnings per share of the past; however, Forward PE Ratio is calculated using the forecast earnings per share. Please see below an example of Trailing PE vs. forwarding PE Ratio.

- Trailing Price Earning Ratio formula = $234 / $10 = $23.4x

- Forward Price Earning Ratio formula = $234 / $11 = $21.3x

For more details, have a look at Trailing PE vs. Forward PE

Question #13 – Can Terminal value be Negative?

This is a tricky equity research interview question. Please note that it can happen but only in theory. Please see the formula below for Terminal Value.

If for some reason, WACC is less than the growth rate, then Terminal Value can be negative. High growth companies may get negative terminal values only due to misuse of this formula. Please note that no company can sustain growth at a high pace for an infinite period. The growth rate used here is a steady growth rate that the company can generate over a long period. For more details, please look at this detailed Guide to Terminal value.

Question #14 – If you were a portfolio manager with $10 million to invest, how would you do it?

This equity research interview question is asked repetitively.

The ideal way to answer this question is to pick a few good stocks large cap, mid-cap stock, & small cap, etc.) and pitch the interviewer about the same. You would tell the interviewer that you would invest $10 million in these stocks. You need to know about the key management executives, a few valuation metrics (PE multiples, EV/EBITDA, etc.), and a few operational statistics of these stocks to use the information to support your argument.

Similar types of questions where you would give similar answers are –

- What makes a company attractive to you?

- Pitch me a stock etc.

Question #15 – What PE ratio of a high-tech company is higher than the PE of a mature company?

The basic reason for which the high tech company’s PE is higher is that the high tech company may have higher growth expectations.

- Why is it relevant? Because the expected growth rate is a PE multiplier –

- [{(1 – g)/ROE}/(r – g)]

- Here, g = growth rate; ROE = Return on Equity & r = cost of equity.

It would help if you used a PEG Ratio for high-growth companies instead of a PE Ratio.

Question #16 – What is BETA?

This is among the top 5 most expected equity research interview questions. Beta is a historical measure representing a tendency of a stock’s return compared to the change in the market. Beta is usually calculated by using regression analysis.

A beta of 1 would represent that a company’s stock would be equally proportionate to the change in the market. A beta of 0.5 means the stock is less volatile than the market. And a beta of 1.5 means the stock is more volatile than the market. Beta is a useful measure, but it’s a historical one. So, beta can’t accurately predict what the future holds. That’s why investors often find unpredictable results using beta as a measure.

Let us now look at Starbucks Beta Trends over the past few years. The beta of Starbucks has decreased over the past five years. This means that Starbucks stocks are less volatile than the stock market. We note that the Beta of Starbucks is at 0.805x.

Question #17 – Between EBIT and EBITDA, which is better?

Another tricky equity research interview question. EBITDA stands for Earnings before interest, taxes, depreciation, and amortization. And EBIT stands for Earnings before interest and taxes. Many companies use EBITDA multiples in their financial statements. The issue with EBITDA is that it considers the depreciation and amortization as they are “non-cash expenses.” So even if EBITDA is used to understand how much a company can earn, it still doesn’t account for the cost of debt and its tax effects.

For the above reasons, even Warren Buffett dislikes EBITDA multiples and never likes companies that use it. According to him, EBITDA can be used where there is no need to spend on “capital expenditure,” but it rarely happens. So every company should use EBIT, not EBITDA. He also gives examples of Microsoft, Wal-Mart & GE, which never use EBITDA.

Question #18 – What are the weaknesses of PE valuation?

This equity research interview question should be very simple to answer. However, there are a few weaknesses of PE valuation, even if PE is an important ratio for investors.

- Firstly, the PE ratio is too simplistic. Just take the current price of the share and then divide it by the company’s recent earnings. But does it take other things into account? No.

- Secondly, PE needs context to be relevant. If you look at only the PE ratio, there is no meaning.

- Thirdly, PE doesn’t take growth/any growth into account. Many investors always take growth into account.

- Fourthly, P (the price of share) doesn’t consider debt. As the market price is not a great measurement of market value, debt is an integral part of it.

Question #19 Let’s say that you run a Donut franchise. You have two options. The first is to increase the price of each of your existing products by 10% (imagining that there is price inelasticity). And the second option would be to increase the total volume by 10% due to a new product. Which one should you do and why?

This equity research interview question is purely based on economics. So you need to think through and then answer the question.

First of all, let’s examine the first option.

- In the first option, the price of each product is increased by 10%. As the price is inelastic, there would be a meager change in the quantity demanded, even if the price of each product gets increased. So that means it would generate more revenue and better profits.

- The second option is to increase the volume by 10% by introducing a new product. In this case, introducing a new product needs more overhead and production costs. And no one knows how this new product would do. So even if the volume increases, there would be two downsides – one, there would be uncertainty about the sales of the new product, and two, the cost of production would increase.

After examining these two options, the first option would be more profitable for you as a franchise owner of KFC.

Question #20 – How would you analyze a chemical company (chemical company – WHAT?)?

Even if you don’t know anything about this equity research interview question, it’s common sense that chemical companies spend a lot of their money on research & development. So, if one can look at their D/E (Debt/Equity) ratio, it would be easier for the analyst to understand how well the chemical company utilizes its capital. A lower D/E ratio always indicates that the chemical company has strong financial health. Along with D/E, we can also look at Net Profit margin and P/E ratio.

Video Explanation Of Equity Research

Recommended Articles

This article has been a guide to Equity Research Interview Questions. Here we provide you with the list of most common techniques and nontechnical equity research interview questions with answers. You may have a look at these other recommended resources to learn more –

- Equity Research Analyst

- Equity Research Jobs

- Equity Research Careers

- Careers In Equity Research Analyst

- Research Associate

Prepare well and give your best shot. All the best for your Equity Research interview!